Monetisation In Video Games

Gaming is one of the most massive industries out there, with it being evaluated at $178 billion in 2021, and it is estimated that it will amount to $268.8 billion in 2025. Games aren’t just for entertainment, they are played for a variety of reasons such as competition, socialising with friends, and more. With games being so universally popular and a lot of popular ones like Candy Crush for mobile or Fortnite for PC/console/mobile being free, the question that arises is, why do companies keep investing in it? How do they make money from it and keep their industry thriving while also creating new content for their audience? The answer to that is game monetisation.

Game Monetisation at a Glance

Video game monetisation is a type of process that a video game publisher or developer can use to generate revenue from a video game product. The methods of monetisation may vary between games, especially when they come from different genres or platforms, but they all serve the same purpose: to return money to the game creators, copyright owners, and other stakeholders.

Initially, game monetisation was pretty simple: you’d pay a fixed fee to get hold of a physical copy of a game, or go drop a quarter in an arcade for one more turn. But with different kinds of games and gaming platforms popping up, there are several kinds of monetisation methods, each with their own set of pros and cons.

A lot of games still can be bought with a one-time fee, such as the Assassin’s Creed series. These could either be physical discs or digital keys for the game. Some games require a subscription on a recurring basis to play such as World of Warcraft while others while being buy-to-acquire, are available to play for free through subscription services. A great example of the latter case is the Microsoft Game Pass for PC which not only gives you access to titles but also gives you discounts in the Xbox Store. The share of gamers who currently pay for a monthly gaming subscription worldwide is 35%.

The annual net sum generated by Ubisoft through sales of digital items, seasonal passes, subscriptions, and advertising is €780m. You can also make money through additional content like DLCs and these can be purchased as add-ons to the original game. The annual net revenue generated by Activision Blizzard through microtransactions, DLCs, and subscriptions is $6.49 billion. Finally, a lot of games, especially mobile games, depend on advertisements in-game to generate revenue. These include games like Candy Crush Saga. Mobile games are well on their way to make $39.8 billion in ad revenue alone.

The History of Game Monetisation

Back in the 70s, the most common way to play a video game was to head down to your local game parlor and toss a coin into an arcade machine. Gaming consoles, PCs, and mobile phones weren’t quite in existence yet, and even when they did come into the picture, they were too expensive for most people to buy. Let’s look at the stats for one of the most popular arcade games of all time, Pac-Man.

Cabinets Sold: 400,000 units

Revenue by 1990: $3,500,000,000

Inflation-adjusted: $7,681,491,635

Eventually, in about a decade, computers and consoles became affordable and opened up the retail market. You could buy a game and take it home on a cartridge, floppy disk, and eventually CDs depending on your device. The release of Gameboys and Tamagotchis revolutionised the ability of consumers to game on the go.

Up next came the shareware method where gamers would be able to play a portion of the game for free, and if they liked it, purchase the rest of it later. id Software used this for their famous releases Doom and Commander Keen. This possibly served as inspiration for games that have both a free and premium version where the latter has additional features/levels/content.

Later came DLCs or downloadable content which serve as an expansion or addition to the base game. One of the first ever DLCs was Grand Theft Auto: London 1969 for Grand Theft Auto and was a resounding success. Games like Total Annihilation in 1997 also offered a new unit every month as free downloadable content for the game on PC. In fact, more money is now spent on DLCs and subscriptions compared to buying video games themselves in the US according to data from 2021.

Of course, once mobile gaming came into existence, so did the Apple App store and the Android Playstore. Initially, most apps were paid for with a one-time fee but then the F2P methods and freemium versions also slowly gained popularity. You can read more about this and the history of mobile gaming in our comprehensive article.

As for PCs and consoles, online gaming expanded. Back in the late 90s and 2000s, F2P games came into existence with the revolutionary notion that a game could be completely free for everyone, that purchases didn’t give their players an advantage in the game. Games like Neopets, Runescape, and Maplestory gained popularity for these reasons, and even today in newer games, you can buy cosmetic items which make you look cooler than ‘default skin players’, such in the case of Fortnite, which generated $9 billion in revenue in its first two years.

The concepts of subscription gaming, in-game items, then loot boxes also gained traction over the past two decades. The concept of in-game items was cemented with the release of ‘horse armor’ packs for Bethesda Softworks‘s The Elder Scrolls IV: Oblivion in 2006, and subsequently followed by many similar content packs over the next few years. Microtransactions and in-app purchases (IAPs) also became a considerable source of revenue in the upcoming years.

In-game advertisements also took off around the mid-2000s, particularly on mobile devices. It is estimated that in-game ad revenue might grow up to $56 billion by 2024. In the last several months, cloud streaming is slowly becoming bigger with more subscription services jumping into the space. You can read about the industry in detail here.

Types of Monetisation

We looked at some types of monetisation which are commonly seen at the onset of this article but different sorts of games and platforms prefer various kinds of monetisation methods. For example, most mobile games use free-to-play (F2P) models with inbuilt advertisements or in-app purchases (IAPs) for generating revenue. There are also mobile games that work on the freemium model where you get free but restricted access to the game before you need to buy the full premium version of the game to unlock the rest of it. The aforementioned model is pretty similar to the shareware approach we’ve covered.

Finally, there are games that are marketed as buy-to acquire but these have dropped significantly over the past decade. In fact, compared to most of the top 10 mobile games in, say 2008, which are accessible with a one-time fee, the top 10 from this year (so far anyway) is comprised of mostly F2P games with IAPs or adverts.

When it comes to mobile games, here are the key types of monetisation seen:

- Buy-to-Acquire games: This is the simplest revenue model. You pay a one-time fee to download a game. An alternative way of doing this is releasing a free version with ads and a premium version with no ads and more content which you can buy with a one time payment. This is how Angry Birds did it on Android. You can also release the first chapter or part of the game for free and then charge for the rest of the game.

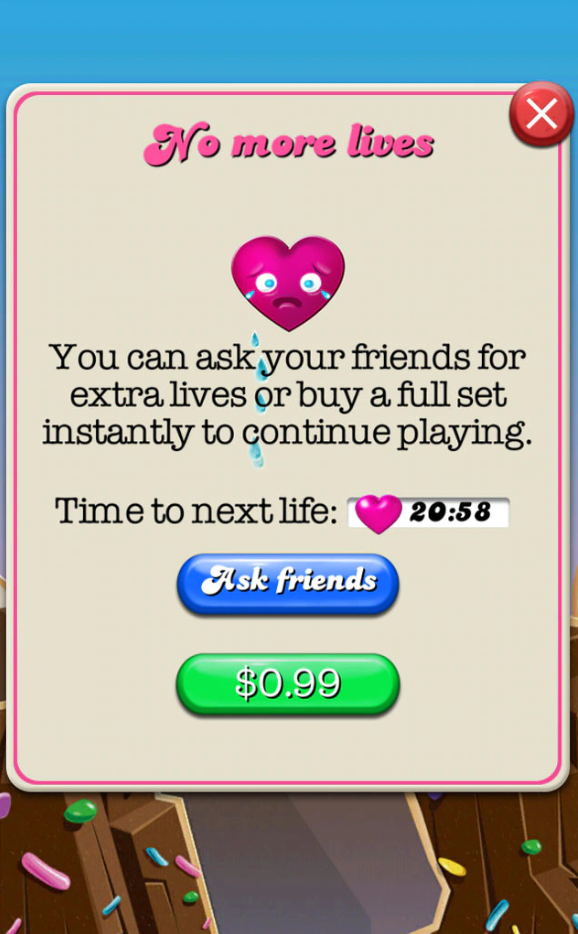

- F2P with In-App-Purchases (IAPS) and Adverts: In this type of game monetisation, the game itself is free which lets the users try them out without having to buy it, increasing the game’s user base. Once in-game, players have the option to purchase in-game perks, abilities, upgrades, or items which help them progress further ahead in the game. A key example of this would be extra lives in Candy Crush Saga. They also have the choice to avoid this and continue playing the game normally. On average, only about 4% of players make a purchase within a game. The players who make these purchases often tend to repeat them and hence are the primary sources of income for the game. When it comes to ads, there are several ways for advertisements to appear in games apart from just the full-screen ads or the banners that appear on the screen headers and footers. Increasingly subtle approaches are being taken by brands such as the sports drink brand Gatorade. They gave players a digital boost through energy refills in EA’s Madden NFL Mobile, letting them play longer. Rewarded ads are currently the leading ad format on mobile. Instead of having an ad forced onto them, players choose to watch a video in exchange for a bonus. Most of these games come with both IAPs and advertisements.

- Subscription models: Games may also have subscriptions that grant the player more items and even on occasion, an edge over normal players, such as VIP Access in games like March of Empires. Games with this form of monetization usually track live data and are updated based on it.

When it comes to console games though, it seems as though the majority preference is still buy-to-acquire games, though subscription services like the Xbox Game Pass are still popular. Within consoles, there is an internal war as to which console sells better. This used to be between the Xbox and the Playstation, though in the past two years, it’s the Nintendo Switch which has sold the most. This could be a result of the several Nintendo exclusives like Animal Crossing: New Horizons and Super Mario Odyssey. Between the Xbox and Playstation though, it is still the Playstation coming out on top. A large portion of this success can be attributed yet again to the exclusive games available on the Playstation platform such as The Last of Us or the Uncharted series. When most people would only want to own one console, these exclusives represent another tangible benefit for investing in one particular console. However, exclusives are slowly fading away, and you can read more about that in this blog.

Looking at console subscription services, Microsoft and Nintendo are doing a phenomenal job of making these appealing to their audience. The former offers Game Pass, which is a monthly subscription providing all-inclusive access to Xbox games and new games. Customers get access to more than a hundred Xbox games—including previous generation games that played on Xbox, Xbox 360, Xbox One, and Xbox Series X. Game Pass subscriptions are also available for use on PCs and mobile devices that support cloud play so that you can play compatible games available through the Game Pass on other devices. This last point in particular has hugely popularised the Game Pass and even people without an Xbox often buy it so they can play on other devices, usually the PC.

The Nintendo Switch Online subscription service provides access to more than 100 games from Nintendo and Super Nintendo, including the classics Super Mario Brothers and Donkey Kong Country. The company also offers an expansion pack with more enhanced services, including cloud saving and online multiplayer. Last month, Sony released their answer to Game Pass called Playstation Plus Extra and Premium. They follow the same model as Game Pass and provide a large library of both current generation games and older games from the PS2 and PS3 as well. One major issue in Nintendo games which the Online subscription is partially remedying is how the same game needs to be bought separately on each different generation of Nintendo devices.

When it comes to PC games, buy-to-acquire games and in-game transactions are the forerunners for preferred methods of monetisation, followed by subscription services for either games like Humble Bundles or cloud gaming subscriptions like Nvidia’s GeForce Now and Google’s Stadia. Lots of players still like buying physical or digital copies of a game. When it comes to online games, especially free ones, in-game advertising similar to mobile games plays a role. Finally, a recent kind of monetisation called play-to-earn, where both the players and the game publishers profit, is gaining traction with the rise of the Metaverse and games like Axie Infinity. Axie Infinity has made over $4 billion in NFT sales since its launch. It also shows that there have been 14.45 million transactions and 1.62 million buyers since its inception.

Apart from our breakdown across devices, here is a comprehensive list of game monetisation methods employed by game makers before and after a player has acquired the game.

1. Pre-Acquisition:

These are monetisation methods usually employed before you purchase a game or a subscription to it.

Pay-per-Play

Like the name suggests, you pay per game. This originated during the time of arcade machines where one game cost a quarter or two to play, and apart from online games like Poker or Rummy where you have to buy-in per game, it is not that popular these days.Buy-to-Play

Like premium games, the consumer buys the game once to play, but here, the game generally continues to be supported by the developer or publisher by maintaining online servers or producing new content regularly for the title. Examples of games like this include GaaS titles such as Rainbow Six Siege and Minecraft.Free-to-Play

Free-to-play games do not require the player to purchase the title to play, though access to some features and content may require purchase of a subscription or via microtransactions. An example of this would be Angry Birds, which after being a paid app on the Apple App Store, shifted to a freemium model where to unlock extra levels and play unhindered by ads, you needed to make a one-time payment. There are subtypes here as well, which you can see below:

– Truly Free: The game is free and you don’t need to buy anything to complete playing it or to win. Games like Pixel Dungeon which have no ads or strings attached come under this category. These are not made for monetisation purposes, they are created and put out into the world by developers who want to express their artistic vision.

– Freemium/Shareware: Games that have a demo version or come with restricted content come under these categories. For freemium games, the aforementioned Angry Birds is a great example. Shareware is another, rather dated method of game monetisation where the games are free to play to start, but limit how far the player can progress before they must purchase the game. You could play the first part of a game, and if you liked it, you could buy the rest of it. Games like id Software’s Commander Keen or Doom were sold and marketed in this way.

– Free to play games with IAPs: These are games which are free to download and play, but come with in-app purchases (IAPs) such as in-game skins (Fortnite), extra lives and hints (Candy Crush Saga), and the like. These are popular because such games thrive on a small minority of big spenders. According to App Annie, games now compose 56% of all App Store spending, with 95% of this on IAPs.Subscription model (Pay-to-play):

These are games that require the player to pay a regular subscription fee to maintain access to all parts of a game. The game is typically free-to-play to allow new users to try the game but full access requires the subscription to be paid. A good example of this is Destiny. Other examples of this include games like World of Warcraft, which is free to play up to level 20, after which you need to buy a subscription.

These can be further split into the following:

- Subscription Model

For these kinds of games, you need to pay a monthly or annual subscription fee usually to be able to access the entire game with all its features. You might also have in-game transactions but a majority of the revenue for these kinds of games comes from the subscription fee. - Subscription Services

These are services through which a gamer can gain access to a multitude of games for a fixed monthly price. The player may need to buy access to new content at times, such as through a season pass. This includes both offline stores as well as digital distribution methods. The best example of these is the Xbox Game Pass or Apple Arcade.

Games can be bought either through retail outlets offline or through digital distribution methods. The former are growing less popular with digital distribution being instantaneous, less onerous since you don’t have to find a place that stocks a game before heading there to buy it, and cheaper since digital copies of games are often cheaper, though not always, compared to physical ones.

2. Post-Acquisition:

Downloadable Content (DLC)

These include additional pieces of story, new areas, and weapons added to the game, new characters, and the like. These can be purchased with an ultimate edition of the game or bought separately if released after the main game. Examples of great DLCs include Blood and Wine for Witcher 3: Wild Hunt or the Citadel DLC for Mass Effect 3.

Season Passes

A season pass is a form of DLC Compilation in which consumers purchase a package for current and future downloadable content (DLC) packs for a video game (that is generally cheaper than the base price of purchasing DLCs individually). A game may have a single season pass or, for some GaaS games, new season passes over time. Examples include Assassin’s Creed Valhalla’s Season Pass and Super Smash Bros. Ultimate: Fighters Pass Vol. 2.

Microtransactions or IAPs

We briefly spoke about how IAPs can be found in F2P games and act as their monetisation method but these can also be present in paid games. In fact, Star Wars Battlefront 2 had to remove game-play affecting microtransactions which made the game pay-to-win. Players no longer had to pay to unlock characters though microtransactions for in-game cosmetics still stayed.. However, microtransactions when they don’t mess up gameplay by giving unfair advantages or offer enough value for money still exist and work for gamers and publishers alike.

- In-game items:

– Cosmetic Only: These include cosmetics like character and gun skins, house decorations, and the like which don’t provide any benefit to the gamer apart from eye candy.

– Gameplay Affecting: These can be of two kinds, one where by sinking money into the game, one can quickly climb to the top of the leaderboards. The other is by purchasing things like hints or extra lives so that you can solve the game when you’re stuck as opposed to propelling you forward. If gameplay-affecting IAPs are excessive, the game becomes unplayable for free players and the user base of the game will greatly decrease. - Loot boxes:

A loot box is a consumable virtual item which can be redeemed to receive a randomised selection of further virtual items, or loot, ranging from simple customization options for a player’s avatar or character, to game-changing equipment such as weapons and armor. A loot box is typically a form of monetisation, with players either buying the boxes directly or receiving the boxes during play and later buying “keys” with which to redeem them. These can be seen in games like Rocket League (which removed them two years ago) and Genshin Impact (there till date.)

Some loot-box systems within free games are criticised as “pay-to-win” systems. In these cases, the contents of the loot box contain items, beyond superficial customization options, which directly affect gameplay, such as booster packs for a digital collectible card game. An example of this is Hearthstone, where players have to keep spending money to get new cards. Full-priced games which already provide downloadable content and then include a loot-box system have been heavily criticised by players. One of the games which drew a lot of flak for this was the aforementioned Star Wars Battlefront 2. The outcry against loot boxes has reached the ears of international lawmakers and they’ve already created legislation which has pushed some countries to roll out bans, like Belgium. - VIP Subscriptions:

These are a kind of special subscription, usually on top of purchasing a game or subscribing to it which offers exclusive rewards that give your game a boost and make you stand out. For example, if you purchase the VIP subscription for Forza Horizon 5, you will receive 3 Exclusive Forza Edition cars, Vanity Items, 2x Credit race rewards, weekly bonus Super Wheelspins, and loads more. - Battle Passes:

Again, you can buy these in game, usually F2P games. They encourage players to play the game on a periodic basis to complete it while also providing them with in-game items and cosmetics they can use. Games like Fortnite and Valorant have these.

Advertisements:

When it comes to in-game advertisements, they can be of two major kinds:

– Interstitial ads

These are ads which are initiated by the game and cannot be avoided by the player usually. These include popups which players have to watch for a few seconds before closing or ads that appear along the foot or side of the game while playing. These are usually simpler to make while also more annoying to the player, unless they’re interactive or creative. Gameloft worked with Indian online retailer Myntra for a playable ad campaign that received an impressive 82% completion rate and 2.1 million impressions in just under two months.

– Reward ads

These are ads which are initiated by players, usually for additional resources like more in-game currency, extra lives, or faster cooldowns. These are usually more accepted by players since they have a choice as to whether they want to watch them while also being rewarded if they do.

Play-to-earn Games:

These are games that typically incorporate blockchain elements such as NFTs. Players are incentivized to use NFTs to improve their existing portfolio or create new NFTs, with their sale managed by the video game publisher or developer. The player then is paid by the company for their work towards the new and/or upgraded NFT. Games like Axie Infinity have even proven to be a source of revenue for some players but these games are also rather susceptible to scams.

There is usually an upfront payment required by the player to get started, typically in the purchase of either cryptocurrency used by the game or in-game currency that they can later trade out, thus making these games “pay-to-earn”, and have been considered the equivalent of Ponzi schemes.

The Impact of Monetisation

At the end of the day, the video game sector is also an industry expected to continue generating the incredible revenue which it does. This means that in order to get gamers to spend more time and money on their games, publishers and developers alike will need to innovate and hold themself to a certain standard. In fact, with developers investing more time in games post their launch to ensure they remain fresh, players often end up getting more value for their money. A great example of this is the original Destiny. Games which were initially pay-to-acquire have also been made free and have switched to an IAP-driven revenue model. The Epic Games store in particular is driving this transition with their acquisition and subsequent free giveaways of games like Rocket League, Among Us, and Fall Guys.

However, monetisation of games can also come with negative impact for games. Since the method of monetisation must be decided before the game production, it may affect the game’s overall design and will shape how new games are designed. This might mean that games might be made in genres that are easier to monetise. Copies of successful games flooding markets can also lead to a lack of originality. For example, the F2P game Wordle has a plethora of similar games, some good and some bad. The rush to make the most money from one’s game can also lead to an improper consideration of balance between good game design and effective monetisation. This in turn can cause either players feeling extorted by the game and its developers or a failure of the game to produce enough revenue for the game to turn a profit.

Finally, with games shifting towards a digital world, the question of ownership comes into play. Ubisoft recently said Assassin’s Creed Liberation from Steam would be removed and players who had bought it through that portal couldn’t access it even though they, according to Steam, owned the game. This was eventually rolled back and the game was made available again after global outrage. This is however a reminder that licensing issues can arise anytime and if they strike owners of digital copies, well, odds are that they won’t be able to play the game again. Also, with servers going down for decrepit games, they can become unplayable as well.

To conclude, in our previous blogs about the game industry, we look into the motivations of players and how the decisions they make regarding platform players, investment in the metaverse, and futuristic tech like VR and cloud gaming. All of these usually incorporate monetisation in some form or the other. When it comes to monetisation, it seems like the most successful and thriving model by far is the F2P one. Being able to play a great game for free is more likely to encourage a player to buy a battle pass or invest into cosmetics for the game. A great example of this phenomenon are CS:GO and Valorant skins.

One of the best kinds of monetisation methods which benefit both consumers and industry players are advertisements, particularly customer-initiated reward ads. Another method would be subscription libraries where customers get a lot of content and games for a fixed price while publishers can resell older content along with the new. Everyone profits. Whether you want to play a game from the good ol’ days or jump into the latest hit, subscriptions like Nvidia GeForce Now and Xbox Game Pass have you covered across several platforms.

Monetisation has evolved a lot over the years. If you’re looking for custom data about a particular kind of monetisation or the games that fall under the category, we have you covered.

Gameopedia works with clients across the industry on custom requests and can provide in-depth data about metaverse-related games. Reach out to us for data that can empower you to new heights.