Advertising in Video Games

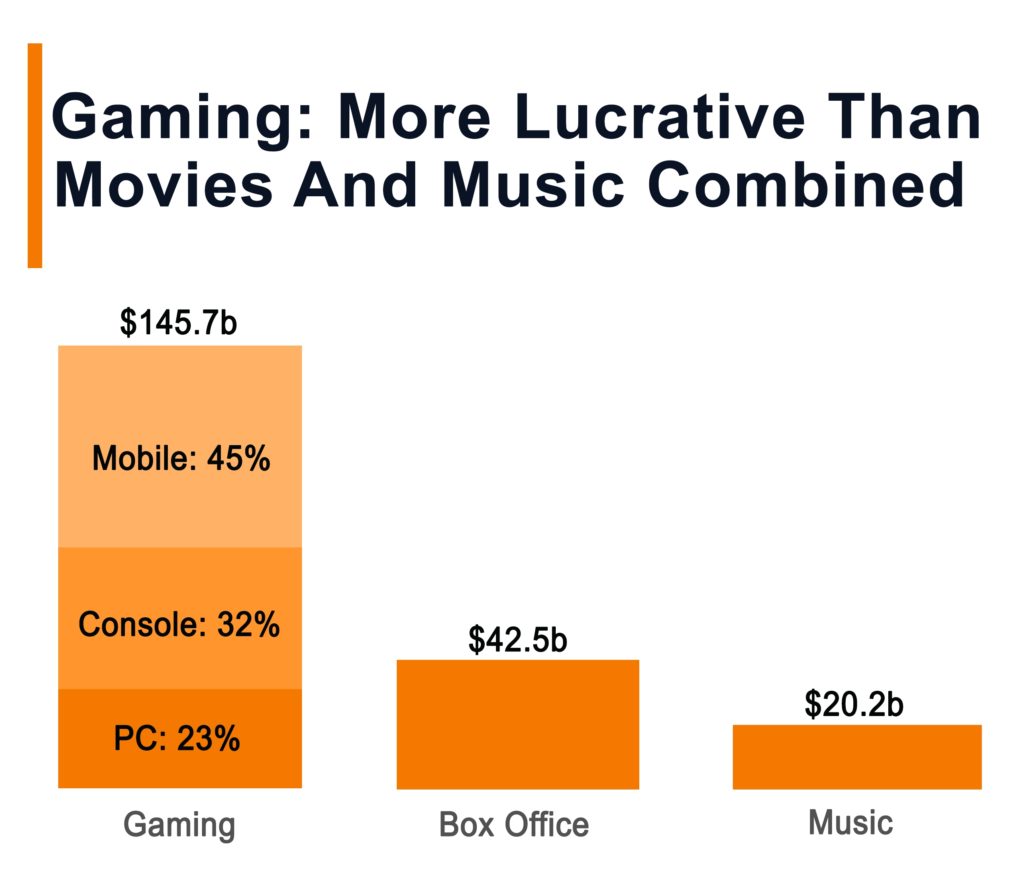

The global market for video games has grown exponentially over the past decade and 2022’s revenue is projected to reach $219.90 billion. This comes from a variety of segments within gaming, which we’ve covered in detail in our game monetisation article. Long gone are the days when game revenue came from physical or even digital sales of copies. These days, subscription services, in-app purchases (IAPs), and advertising all contribute just as much, if not more, to revenue.

The biggest chunk of video game market revenue, a whopping $91.4 billion in 2021, comes from smart-phone games and is more than the PC and console markets combined. In 2019, a survey conducted by deltaDNA found that 94% of free-to-play video game developers incorporate some form of in-game advertising. Knowing these facts, we’re going to zoom in on one particular sector here, which is advertising in games.

It makes sense to look at how advertising in games works and how it came about, considering that the global video games advertising market is expected to reach $4.8 billion by 2024.

The History of Advertisements in Gaming

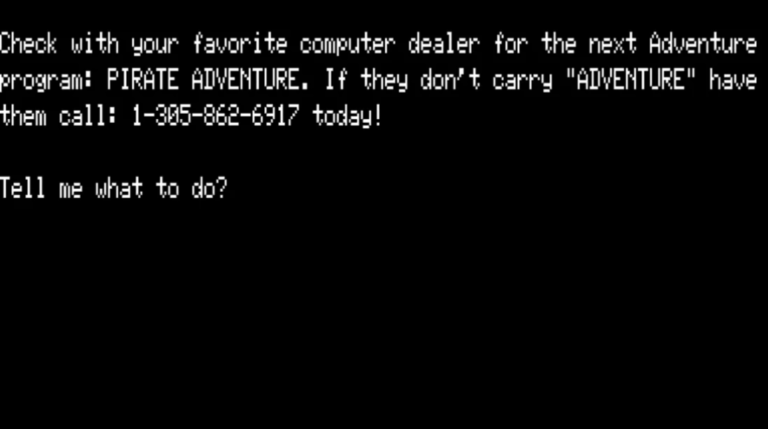

From the above data, the question arises, how did game makers realise the potential of generating revenue through advertising? The first ever ad in-game was actually not a commercial one, but that of a game developer trying to generate interest for his next game. Scott Adams, the creator of Adventureland left a message promoting his next game, Pirate Adventure.

After this (relatively) wholesome ad though, game devs and brands alike took a note from movies and TV shows. They saw how the latter did product placement and wanted to replicate it in games but they faced some hurdles. In movies and shows, you can see the world in great detail so including a product or two doesn’t look odd. A character casually drinking Coca Cola or lacing up their Nike shoes doesn’t affect the quality of the production. In games however, the graphics then weren’t great enough to include most products organically. Thus, the gaming industry came up with another way to partner with brands and those were advergames.

Advergames are games made exclusively for advertising purposes. The first released advergame was Tapper in 1983. The game had been originally sponsored by brewer Anheuser-Busch, and featured the brand’s logo with gameplay based on serving beer. The game proved so popular that a non-branded version of the game, Root Beer Tapper, was released for general arcades, with the beer replaced by root beer to cater to younger audiences. In the 80s and 90s, numerous advergames were released (though the term only came into existence in 1999) and with graphics improving significantly, new advergaming opportunities appeared. For instance, car manufacturers couldn’t really show off their cars in games until graphics improved enough by the 90s and games like Driver and Need for Speed really took off (though they didn’t show these vehicles being damaged even if you were an awful driver because bad for business, but we digress.)

While ads these days in games are mostly annoying, back then, a lot of the released advergames were actually quite popular and… fun. Chex Quest, a cereal-themed child-friendly remake of Doom, was a huge hit and is till date, considered one of the best advergames made. Advertisers also experimented with different kinds of product placements. They had ads integrated into splash screens (McVities Penguin Chocolates in James Pond Robocod, 1991), they made their mascots characters in-game to avoid directly mentioning their products (Ronald McDonald starring in McDonald’s Treasure Land Adventures, 1993), and they even weren’t below taking potshots at their competition. The latter in particular was interesting: Coca Cola worked with Atari to redesign their mega-hit Space Invaders for one of Coca Cola’s sales conventions. The aliens you had to shoot would spell out ‘Pepsi’ on the screen. A rather on the nose shot.

In 1999 though, Crazy Taxi rewrote the classic advergame template, where the brand was no longer the center of the game but instead, just a facet. In the game, you’re a taxi driver picking up a passenger and taking them to where they want to go, which are places like Levi’s store or Pizza Hut. You could also see other brands and stores enroute, and the placement of all of these were organic enough for gamers to appreciate the realism. A case of where art imitates life (a tad ironically) arose in games like Madden, NFL, and FIFA. They all had to pay licensing fees to incorporate details from the real-life leagues and to offset these, they started getting into sponsorship deals with brands to show them prominently in-game.

In 2005, a game called Splinter Cell: Chaos Theory used what we call now as ‘dynamic advertising’ where the ads shown were relevant to players. This audience segmentation, as it is known, was first done by Splinter Cell’s developers Ubisoft, though the industry followed suit soon.

Of course, if you’re going to be overly heavy handed with in-game product placement, especially if it doesn’t make sense in the game universe, your audience isn’t going to be very happy about it. EA found this out to their chagrin when their billboards for Pepsi and Intel in Battlefield 2142, a game supposedly set a century in the future, were disliked strongly by players. To give them their due, they did eventually remove the ads from the game but it was one of the first games where the negative side of putting ads in your game really showed up.

When mobile gaming started to take off, it led to a change in game design and how games were monetized. Games were now often F2P with their main revenue coming in from ads. We’ve covered how exactly mobile games are monetized in our article about them if you want the details, but a lot of different kinds of ads began being made and incorporated into games. We’ll head into the different types of ads in a later section but suffice to say, ads in games were here to stay. However, not all game developers took care that these ads were ok with their customers. Often, mobile games have the issue of showing too many ads. You clear a level? Ad. Lose a life? Ad. Open the app? Ad. This sort of nagging by a game would be bad enough but since a lot these games derive most if not all of their revenue from ads, they feel the need to make levels shorter and squeeze in as many adverts as possible to maximise revenue, to an extent sometimes where games become almost unplayable.

Finally, both AR and VR have also started seeing the potential of ads to generate revenue. In Pokemon Go, Niantic added advertising which showed up depending on which location you were at, bringing the real and virtual world together. While there are no conventional banner ads in Pokemon Go, they still have sponsored Poke Stops, free items in-game from companies that support the game which you can claim by looking at an ad, and even some sponsored cosmetics but so far, all of these have not messed with the game’s immersion. On the VR side of things, Volvo made an app that uses VR glasses to test drive their XC90 SUV. In fact, by 2022, the number of annual installs of AR and VR apps will grow by 45% compared to 2017, and the market for in-app purchases will increase by 92%.

The Types of In-Game Advertising

We can see from our history of game advertising that there are several ways of placing products in-game. Different methods of advertising work for various products, game devices, or even game genres, and especially with mobile game ads, a lot of variety has popped up. Let’s look at the major types.

Static Advertising/Product Placement:

Static in-game advertising is when ads are coded right into the game and can’t be changed (unless the game is completely online.) These advertisements are planned and integrated into a video game during the design/development stage, and as such, can be integrated in a customised manner. For example, Splinter Cell used in-game Sony Ericsson phones to catch terrorists. Unlike conventional static advertising in real life, static ads in game allow players to interact with the product being advertised. Ads are also incorporated on billboards, especially in sports games, analogous to how it happens in reality.

- Advergames:

These are custom-made games which are built for promoting a particular product or brand through its story, environment, or gameplay. Advergames can also offer players benefits in real life through coupons, discounts, and the like. These games are a fun and entertaining way for brands to connect with their customers if done right.

Examples of great advergames include Cool Spot from 7up, Sneak King by Burger King – this led to a 40% increase in sales revenue for Burger King, McDonald’s Treasure Land, and Pepsiman by, well, Pepsi. - Dynamic In-Game Advertising

Dynamic advertisements are those which consider various factors such as location, age, personal interests, and more before displaying ads. These are personalised ads at scale and using dynamic ads, any brand can segment people who use their app or website and show them products and services they have a keen interest in. They allow game developers/publishers or the ad delivery service to track their ads in real-time and get data such as angle from which the ad is viewed, screen-time spent, and more to correct issues and improve existing and future ads.

There are various kinds of dynamic ads, some of which include:

- Diegetic dynamic ads: These are dynamic ads which are seamlessly placed in the video game world. This allows media buyers to purchase real-time and geo-targeting capable advertising inside of video games. The adverts appear inside the game environment, on virtual objects such as billboards, posters, and bus stops – all of which are objects that you’d expect to see in a realistic sports or urban environment video game. Tony Hawk: Ride is an example.

- Interstitial ads: According to Google, interstitial ads are full-screen ads that cover the interface of their host app. They’re typically displayed at natural transition points in the flow of an app, such as between activities or during the pause between levels in a game. When an app shows an interstitial ad, the user has the choice to either tap on the ad and continue to its destination or close it and return to the app, though often, games force users to sit through several seconds of the ad which can be quite frustrating. Video ads are a popular kind of interstitial ad in games.

- Banner Ads: These are advertisements present in the form of banners in the game. They may be displayed at different positions like the top, bottom, or side of the screen. They may occur at different instances in the game such as in the main menu, during gameplay, between levels, and more.

- Reward ads: These are ads which are basically an in-game exchange offer: users view ads for in-game rewards like extra lives, boosters, and the like. Candy Crush is a good example of a game with good reward ads. Since these ads are optional and users can choose to avoid them, they aren’t as negatively looked at and they even increase in-app purchases. However, unlike interstitial video ads, some of these are not skippable.

- Playable ads: These are mini games users can try out and if they like it, they can install the complete app. They make for a great user experience and have some of the best conversion rates. Tennis Clash and Royal Match both are popular playable ads.

- Offerwall ads: These tend to list out tasks that users can complete in exchange for in-game rewards. They act almost like a mini online store and since they’re optional, they aren’t frowned upon as much as ad barrages. They also increase time spent on apps significantly by extending the session length.

- Through-the-Line Advertising

This is a kind of advertising that involves the use of URL hyperlinks within the game to get players to visit web-pages with advertisements. The technique used to tempt the player into visiting the intended URL varies from game to game.

In games such as Enter the Matrix, Year Zero, I Love Bees, and Lost Experience, URLs make up a part of the background of the game such that certain plot details can only be learned by following the link.

Why Ads are a Necessary Evil

Advertisements have their benefits (at least for game development companies and the companies placing the ads) but they have more than their fair share of issues. While ads are great in a way that they keep games F2P, especially when it comes to mobile games, they can often prove to be extremely annoying, tasteless, or even downright misleading. Let’s look at the good, bad, and ugly when it comes to in-game advertising.

Pros:

- The biggest point in the favour of advertisements in-game is that they can create new revenue streams. By adding ads to games, companies can reduce the price they’re sold at, and even make them free, as seen by the F2P model pioneered in mobile devices. When Angry Birds was ported to Android devices, it was released as a free game with ads and even if users opted not to pay to remove ads, they could still enjoy the game. King’s release of Candy Crush Saga as a F2P game right off the bat propelled it to the top of the charts. In just more than a year, King had seen over 400 million new players of the game and their revenues had jumped from $62 million in 2011 to $1.88 billion from advertising revenue and in-app purchases.

- In-game ads which promote a popular artist or concept can also boost your own game. For example, in 2021, Fortnite announced the continuation of its cooperation with the Jordan brand. Players can compete for the Air Jordan XI Cool Gray, the iconic sneaker model, and discover rooms dedicated to the best basketball players. The MVP gets access to a virtual museum, a basketball court to test your abilities and an immersive video that advertises the Jordan brand.

- A 2009 study by an advertising company found that 80% of consumers correctly recalled an advertiser and 56% had a more favorable impression of the advertiser because it allowed them to play a free game. This is especially relevant when it comes to advergames and mobile gaming, though in the past decade, it’s more of the latter. FIFA and other popular licensed sports franchises made extensive use of in-game product placement and advertising, on billboards, jerseys, and more. Since these franchises already have a great deal of sponsorships and ads in real life, in game, it didn’t cause eyebrows to be raised.

- In-game advertising is an important source of income for browser-based and other Internet games that do not feature micro-transactions or pay-to-play. Websites like miniclip, pogo, and kongregate all feature free games one can play online and they offset their expenses with ad revenue.

Cons:

- Integrating IGA into games without alienating or frustrating players can be hard, especially if done overtly. A lot of mobile games tend to slam ads between every level, if you fail a level, and as soon as you open or close the game. They also tend to shorten levels to increase the number of ads opened and this can make playing them really frustrating.

- Some games market themselves as something they aren’t: titles like Homescapes which is basically a match-3 puzzle game is peddled as, well, a fixer-upper game in ads. This kind of misrepresentation leads to a lot of downloads but it also causes games to look at mobile titles with increasing resentment and scepticism. This is more of a marketing issue than being specific to ads.

- Game companies and developers worry that they may be forced to change the game as requested by advertisers if in-game adverts become a common revenue source, and face a possible backlash from consumers. However, certain kinds of ads, such as reward ads are actually looked at favourably by users and removal of them can lead to customer dissatisfaction.

- Like in any other industry, false advertising is an issue in games as well. In one rather notable instance, the Gatorade company had published a free mobile game Bolt! which featured Usain Bolt and challenged the player to “keep your performance high by avoiding water”. The state of California asserted this claim was false, as Gatorade had been shown to be more harmful to the human body than water. Since the game was targeted towards kids and teenagers, this gave the state cause to sue Gatorade. The case was ultimately settled with Gatorade paying a $300,000 fine to the state. This case might have had a happy ending (except for Gatorade). However, misleading claims and even F2P games that promote toxicity are still around. For example, ads on Facebook for a F2P mobile game called ‘Game of Sultans’ literally imply that abuse can make women listen to you. The lack of regulation when it comes to both game making and ads like this can prove deeply harmful.

- In-game advertising can also lead to negative reviews for a video game because the ad doesn’t make sense or just seems very insulting to players. A great example of ads being despised by games was Maxis’ promotion of a heavily branded Nissan Leaf charging station as downloadable content in SimCity. This being the first DLC for the game was just insult to injury.

- Companies have found that gamers do not want distracting advertisements when they have already paid the retail price and/or a monthly subscription fee. Games which are paid, full-on AAA releases already make plenty of money from game sales and having ads which break immersion or are unskippable is not something which customers, for obvious reasons, are gonna be happy about. In NBA 2K20, there were ads during loading screens which are not only unskippable, but also longer than the game load timing. The game already has microtransactions, loot boxes, and cost $60 to get, but this was the last straw for a lot of customers. 2K Games got a lot of backlash for it, but they did the same with NBA 2K21. (Yikes.)

The Future of Ads in Games

We’re in a place where like it or not, ads are here to stay. We’ve looked at both the pros and cons, and at the end of the day, especially when it comes to mobile games, F2P is the monetisation method of choice. Game developers, publishers, and advertisers alike have to find the balance between making enough money and annoying their customers. Innovative ads which provide tangible value to customers is the solution to this. The good news is that players are receptive to ads in-games – in fact, 95% of players say that ads increase in-game realism.

Ad platforms are already connecting publishers and advertisers within the metaverse to deliver in-game ads. Game developers can offer advertisers the possibility to show their ads within metaverse worlds on various fronts such as billboards in stadiums to posters in virtual worlds like Fortnite and Roblox.

Reward-based ads are some of the most successful ones: they have been shown to directly increase in-app purchases, increase screen-time, and improve engagement. In May 2017, after adding rewarded video ads that enabled users to gain an additional life, CookApps saw a 16% increase in session length in one of its apps. A/B testing found that session length shot up by 211% if reward ads were placed as soon as users exhausted their last life. In fact, when Rovio decided to remove reward ads for users who had spent money in their game Angry Birds Transformers, these players were extremely annoyed as they’d come to rely on these ads as a supplement as opposed to an annoyance.

Another reason why advertising in games can be so difficult for game developers and publishers is because they don’t have data often as to what kind of ads their users prefer. This data is often kept secret by the advertiser they tie up with and they’re forced to put in what the advertiser says, sometimes at the cost of user satisfaction. However, if ads which are appealing to their audience based on their preferences are shown dynamically at a frequency that customers can handle based on player data, the irritation these ads cause can be reduced.

Innovative ads are also often appreciated, especially if users get something exclusive. Fortnite is known for their concerts with prominent music artists like Travis Scott and Marshmello but recently, pop star Ariana Grande held a concert in the game across multiple days. While in previous concerts, you could dance in-game with your friends, fly around a giant character model of the artist, and enjoy cool visuals, this time around, you could play minigames where you raced and collected power ups, or fought in-game villains. Experiences like this which are utterly unique are sure to make users happy. With the metaverse booming and online experiences evolving, in-game ads are a great way to make money while also setting a standard and entertaining your users. Finally, sponsorships when done tastefully can be a great way to boost revenues while also advertising a company or product. For example, VALORANT’s international tournaments call rounds where you win by eliminating your opponents without losing your teammates a ‘Prime Gaming Flawless’ as they have a tie-up with Amazon. They also offer free-in game loot for those who have a Prime subscription.

In-game advertising doesn’t have to be something done just for revenue at the cost of annoying your users, it can be done in a way that proves beneficial to all parties involved and that is what both game companies and advertisers should aim for. Data-backed dynamic advertising which either gives users in-game rewards or something else unique is the way to go.

How Gameopedia Can Help You

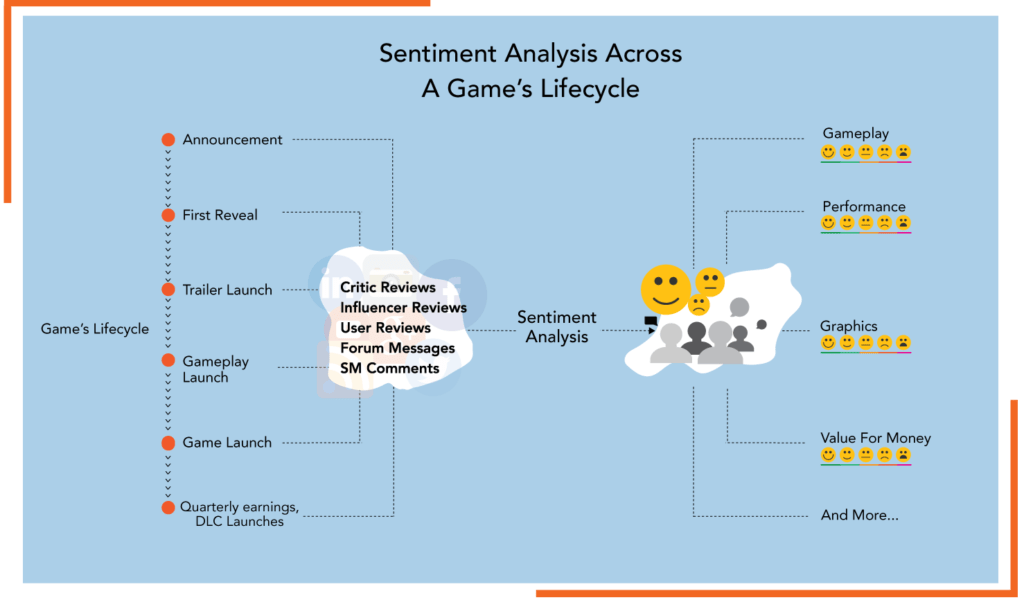

Gameopedia is a company that deeply values data and the impact it can have on games. We can help you improve ad content, targeting, and audience segmentation with detailed, up-to-date video game taxonomy, metadata, and sentiment analysis for games across mobile, consoles, and PC. You can also optimise campaign performance with the right message to the right audience at the right time.

How our data can benefit you:

- You can create impactful display ads with high-quality artwork and videos.

- Improve contextual advertising by targeting the right audience with the right ad at the right time.

- Achieve true hyper-personalization by supercharging audience micro-segmentation.

Reach out to us for data that can empower you to new heights.